DoubleZero Edge: Inside their New Revenue Model

Uncovering the pricing, capacity, and early adoption data behind the shred subscription pivot which could lead to millions in protocol revenue

While sleuthing DoubleZero’s transition from validator fees to Edge, a shred subscription service we uncovered unreleased pricing data that looks like it could lead to tens of millions in revenue at only a fraction of total network utilization. By querying Malbec Labs’ public APIs and cross-referencing onchain data, we uncovered the full pricing structure, current subscriber base, and infrastructure capacity. While the transition has created a near-term revenue cliff, the infrastructure to support tens of millions in annual revenue is already deployed across 29 cities worldwide.

The Pivot: From Validator Fees to Shred Subscriptions

DoubleZero recently eliminated its 5% validator block reward fee at epoch 939, despite it generating ~$3.5M in annualized revenue across 455 connected validators. This revenue funded the protocol’s buyback-and-distribute mechanism where SOL fees were converted to 2Z on the open market, with 10% burned and 90% distributed to infrastructure contributors.

That model is now gone and in its place, DoubleZero launched Edge, a real-time market data delivery platform selling access to Solana shred data via multicast. For context, Shreds are the smallest fragments of Solana blocks, distributed from slot leaders during block building. For traders, searchers, and market makers, shreds represent the earliest observable signal of upcoming onchain activity.

Access to low-latency shred data has historically been dominated by various services like Jito’s ShredStream, Helius, bloXroute, Corvus, and others. Now DoubleZero is positioning itself to compete by leveraging its existing private fiber infrastructure with multicast, enabling them to deliver shreds faster than any of their competitors.

What We Found: Edge Pricing, Capacity & Adoption

Out of the 29 metro codes which currently appear to have devices online, it makes sense that Amsterdam and Frankfurt would both be tier one, as roughly 48% of total Solana stake resides within data centers in those two cities. The Frankfurt links also show some of the highest current utilization of the Doublezero network today.

So What Does this Change in Revenue Model Mean for the 2Z Token?

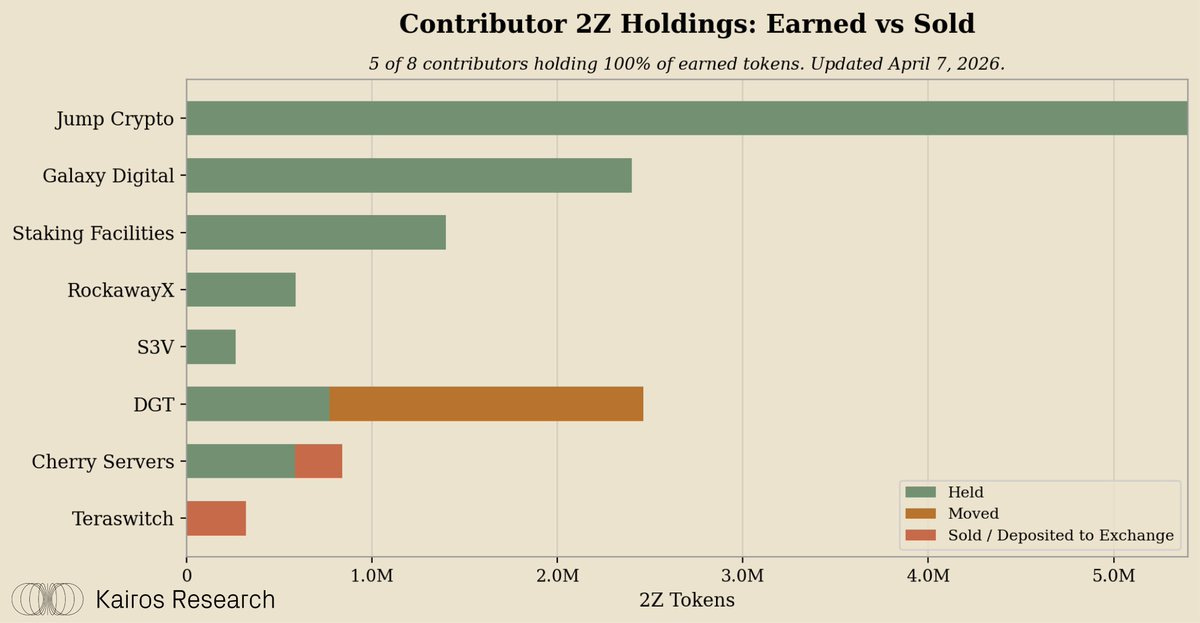

2Z is a token that will live and die by its flows. It’s interesting in the sense that it is truly one of the only tokens that is awarded to contributors on a pro-rata basis, similar to Bitcoin mining, but like Bitcoin miners these contributors are rational economic actors and are profit seeking. In the previous revenue model, fees were accrued from validators in SOL, swapped to 2Z on the open market, and then 10% were burned, and the remaining 90% were distributed to contributors. In the visual below you can see a daily flow of value from the protocol’s inception to date.

Daily flow of protocol revenue from Doublezero to network contributors

We did this by mapping all of the onchain flows, and cross referencing other available data sources to ensure we were tagging wallets correctly. Additionally, mapping these contributor wallets can help us track selling flows. To date, it appears the two primary sellers have been Cherry Servers who conducted onchain sales & Teraswitch who deposited their 2Z to Coinbase.

In DZ’s updated revenue model fiber contributors will see their allocation drop from 90% to 50%, with the remaining 32.5% going to validators, and 17.5% going to protocol client teams (Jito, Harmonic, Triton, etc). The burn rate of 10% will remain consistent as far as we can tell.

What else we noticed through sleuthing the new shredstream program is that the revenue is now collected in USDC vs SOL which we think is good and will lead to less value leakage in the time between the protocol revenue is collected and swapped to 2Z on the open market.

2Z Revenue Multiples

2Z currently trades at a $256M market cap, a 73x multiple on $3.5M annual fee revenue that no longer exists. On actual Edge revenue today, roughly $205K annualized from 13 internal seats, that’s a 1,200x+ multiple, but clearly these are just test txns so that is not a real multiple to consider.

The infrastructure appears to be live. As far as we can tell there are 845 Tier 1 seats at $100/epoch, 1,925 Tier 2 at $60, 5,259 Tier 3 at $30. Here’s what the revenue looks like as those seats fill:

At 5% utilization, roughly 400 seats across the network, Edge matches the old fee model. Every dollar of that revenue becomes a 2Z market buy, with 10% permanently burned. At 10% fill the protocol is purchasing $6.2M of 2Z off the open market annually and destroying $620K of it. Meanwhile, if 2Z continues to clear at an attractive price then more contributors will bring their fiber online and shreds can be distributed faster, making it the superior choice for shred subscriptions as a service, leading to more revenue and more protocol market buys of 2Z. That’s essentially the flywheel.

Closing

DoubleZero walked away from $3.5M in guaranteed revenue to build something with a higher ceiling. Today it looks uncomfortable: 13 seats, one customer, a visible revenue cliff. There has also been verifiable evidence that these are the fastest shreds on the market. See the tweet below for more on that.

Source:

The open risks around 2Z will simply revolve around flows. With the Solana validator count continuously dropping, this new path of shred monetization will be welcomed, but operators are of course going to be selling at least some portion of their rewards. The same can apply for other groups for various reasons. Coins will trade hands, its a natural part of the economic evolution of the network. If you want to keep track of the flows, make sure to follow us, and join our telegram group for alerts of token movement as revenue ramps up and tokens begin flowing to a variety of new stakeholders.